Retiring abroad is about more than choosing a sunny destination. It’s a long-term project involving residency status, healthcare systems, and pension rules — and your insurance decisions need to support you through the transition period, the point at which you start using local services, and any later changes (such as splitting time between countries or moving back home). This guide gives you a practical framework to keep cover continuous, avoid costly gaps, and manage premiums on a fixed retirement income.

Before you rely on local healthcare or cancel any existing policy, confirm the essentials:

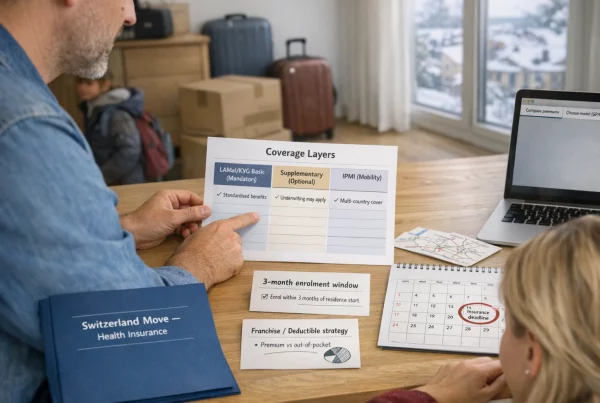

- Visa / residency route, and whether it mandates specific insurance wording (e.g., “no deductible”, an insurer authorised locally, minimum benefits).

- The earliest date you can register for the local public system (and what documents are required).

- How long it takes to activate cover after registration (waiting periods or administrative delays).

- Your plan for “day one” cover on arrival (IPMI, a local private plan, or an employer plan).

- Your renewal dates and cancellation terms — so you don’t accidentally create a gap.

- Where you expect to spend time each year (single country vs multi-country / seasonal living).

- Think 3–10 years ahead: The cheapest option today can become expensive if your circumstances change (health, family, mobility, relocation).

- Eligibility is everything: Public healthcare and pensions depend on residency status, contributions, and treaties — and the rules vary by country.

- Maintain continuity of cover: Don’t cancel existing cover until the new policy is active and confirmed in writing.

- Use IPMI as a bridge and a back-up: IPMI can cover the transition period and fill gaps even after you qualify for public healthcare.

- Budget for premium increases: Premiums typically rise with age and medical cost inflation; build this into your retirement cash flow planning.

- Design your plan to control costs: The main levers are your area of cover, your deductible/excess, and optional benefit modules.

- Portability matters if you’re mobile: Local plans may be excellent for one country, but they may not follow you if you split time or move again.

- Travel insurance is not a substitute: Travel cover is usually emergency-only and often excludes routine and ongoing care.

- Healthcare considerations when retiring abroad

- Eligibility for local public healthcare and pensions

- Role of IPMI during and after public access

- Managing premiums on fixed income

- Portability across multiple countries

- Combining IPMI with travel insurance

- Checklist for retirement planning

- Broker’s role

1. Healthcare considerations when retiring abroad

Moving abroad for retirement means deciding how you’ll access healthcare: the public system, private care, or a mix. A common mistake is assuming state healthcare will be available immediately — but access is often delayed or conditional. That gap is where international private medical insurance (IPMI) (or comparable long-term private medical cover) typically fits.

IPMI is designed for people living long-term outside their home country. Unlike short-trip travel insurance, it is structured for ongoing medical needs (subject to underwriting and policy terms), and it can be portable across borders.

“Public healthcare exists” and “I am eligible for it” are two different things. Eligibility can depend on legal residency, contribution history, treaty rules, and how the country defines “habitual residence”.

Glossary (quick definitions)

A long-term health plan for people living outside their home country, usually renewable annually and valid across multiple countries (depending on area of cover).

The rules that determine when you can use a country’s state-funded healthcare (often tied to residency, contributions, or treaties).

Many healthcare and pension benefits depend on legal residency (and sometimes contributions), not citizenship.

Your ability to keep cover in place when you move between countries or split time across multiple locations.

The annual renewal/anniversary date when premiums and plan options are reviewed. This is often the best time to adjust your plan design.

The amount you agree to pay towards eligible costs before the insurer pays. Increasing the deductible/excess can reduce premium (with trade-offs).

A fixed fee (or percentage) you pay per service/claim, sometimes in addition to a deductible/excess.

Many insurers have provider networks where bills can be settled directly (reducing the need to pay large amounts up front).

Travel policies are typically trip-based and geared to emergencies. They may exclude routine care and often exclude pre-existing conditions.

Common “health cover pathways” (and what to watch)

| Pathway | Typical risks | Common solutions (generic) | Admin complexity | What to verify | Common mistakes |

|---|---|---|---|---|---|

| Before qualifying for local healthcare (arrival + waiting period) | No state cover yet; high out-of-pocket costs if illness/injury occurs | Use IPMI or gap cover; secure a visa-approved policy; confirm the start date on arrival | Medium | Visa insurance requirements, activation date, portability, exclusions | Cancelling existing cover too soon; relying on travel cover for routine care |

| After qualifying for local healthcare (state cover active) | Co-payments, limited benefits, restricted providers, long waits, excluded services | Supplement with private top-up where allowed; keep IPMI for gaps and international travel | Low–Medium | Scope of public cover, waiting times, coordination with private insurance | Assuming “100% free”; not planning for services the public system doesn’t cover |

| Multi-country lifestyle (splitting time / frequent travel) | Gaps outside any one public system; residency/tax complications | Keep one coherent, portable IPMI plan; add local top-ups if needed | High | IPMI area of cover; limits for time in certain countries; residency evidence | Assuming a local plan “travels”; being underinsured outside your primary residence |

| Returning home later (post-retirement move back) | Lapse in cover; delays re-qualifying for the home public system | Keep IPMI as a bridge; plan re-registration; confirm the rules before cancelling | High | Re-joining timelines, paperwork, any gap periods, timing of cancellation | Cancelling international cover early; unexpected waiting periods for public access |

| Seasonal stays (part-year in two places) | Not fully covered in either country; unclear “habitual residence”; travel risks | IPMI that supports split residency; or a local plan + travel cover elsewhere (careful!) | High | How each country defines residence; IPMI rules on alternating countries | Assuming long-stay travel insurance covers months-long stays; mismatched policy dates |

This table is a framework, not a promise. Your actual pathway depends on your visa status, residency timeline, and the country’s rules.

2. Eligibility for local public healthcare and pensions

Each country sets its own rules for overseas residents and retirees. Access to public healthcare usually depends on legal residency and sometimes contributions. Pension entitlement generally depends on your work history and years of contributions.

Public healthcare: what typically drives eligibility

- Legal residency: You may need a residence permit and local registration before you can enrol.

- Waiting periods: Some systems begin after a defined period of legal residence; others require contribution history.

- Habitual residence tests: Countries may look at where you “normally live” (time spent, ties, address, tax status).

- Documents: Proof of address, ID, residency permits, and sometimes proof of income or insurance.

Pensions: contributions, treaties, and “totalisation” concepts

If you have worked in multiple countries, treaties or social security agreements may allow you to combine credits so you can qualify for partial benefits from each system (rules vary by country pair). The calculation and taxation of pensions can be complex and country-specific.

- Don’t assume public healthcare or pensions will “just work” in a new country without paperwork and lead times.

- Verify your exact timeline with official sources (and, if needed, a local adviser).

- Build a bridge plan (often IPMI) for the period between arrival and confirmed enrolment.

3. Role of IPMI during and after public access

Think of IPMI as bridging cover and back-up cover. Before you qualify for public care, IPMI can cover you from day one. After you qualify, you may keep IPMI to fill gaps (for example, private access, shorter waits, excluded services, or protection while travelling internationally).

Before public access begins

- IPMI can give you access to care while you complete residency steps.

- It can reduce financial risk during the “administrative gap” when you’re not yet registered locally.

- It can also support cross-border needs if you travel during your transition.

After public access begins

- You may scale down IPMI benefits to reduce premium once local cover is active (depending on your needs and policy options).

- You may keep IPMI for portability if you expect future moves or seasonal living.

- You may keep IPMI to reduce exposure to long waiting times or limited provider choice in the public system.

Do not cancel existing cover until the replacement is active and confirmed in writing. Administrative delays happen, and being underwritten again later can be harder (and more expensive) than maintaining continuous cover.

5. Portability across multiple countries

If you might move again or split time between countries, portability becomes a core requirement. Local plans may be excellent for living in one country, but they often don’t follow you if your lifestyle becomes multi-country.

What to check for portability

- Territory: Which countries/regions are included or excluded (some plans exclude the USA or limit cover in your “home” country)?

- Residence changes: Are you required to tell the insurer if you change your country of residence?

- Time limits: Does the policy limit the number of days you can spend in certain countries each year?

- Network access: Are there in-network providers where you’ll actually live and travel?

If you’re genuinely mobile, aim for one coherent international plan that matches your likely geography, then add local top-ups only where needed. Constantly switching between local plans can create gaps, increase the risk of further underwriting, and add administrative headaches.

6. Combining IPMI with travel insurance

Travel insurance is typically designed for short trips and usually focuses on emergencies. It is not a like-for-like replacement for IPMI or long-term private medical cover.

When travel insurance helps

- For short trips on top of your main cover (for baggage/trip disruption, and emergency medical as secondary support).

- As a carefully chosen, temporary bridge for emergencies only — if there is a short gap (but read the exclusions closely).

When travel insurance is a risk

- If you are using it for long-term living abroad and you need routine or ongoing care.

- If you have pre-existing conditions and the policy excludes them or has strict disclosure requirements.

- If the trip duration exceeds the policy limit or conflicts with residency definitions.

Treat travel cover as trip-based emergency support — not as your long-term healthcare plan. For extended periods living abroad, use IPMI or a suitable long-term local plan that meets visa and residency requirements.

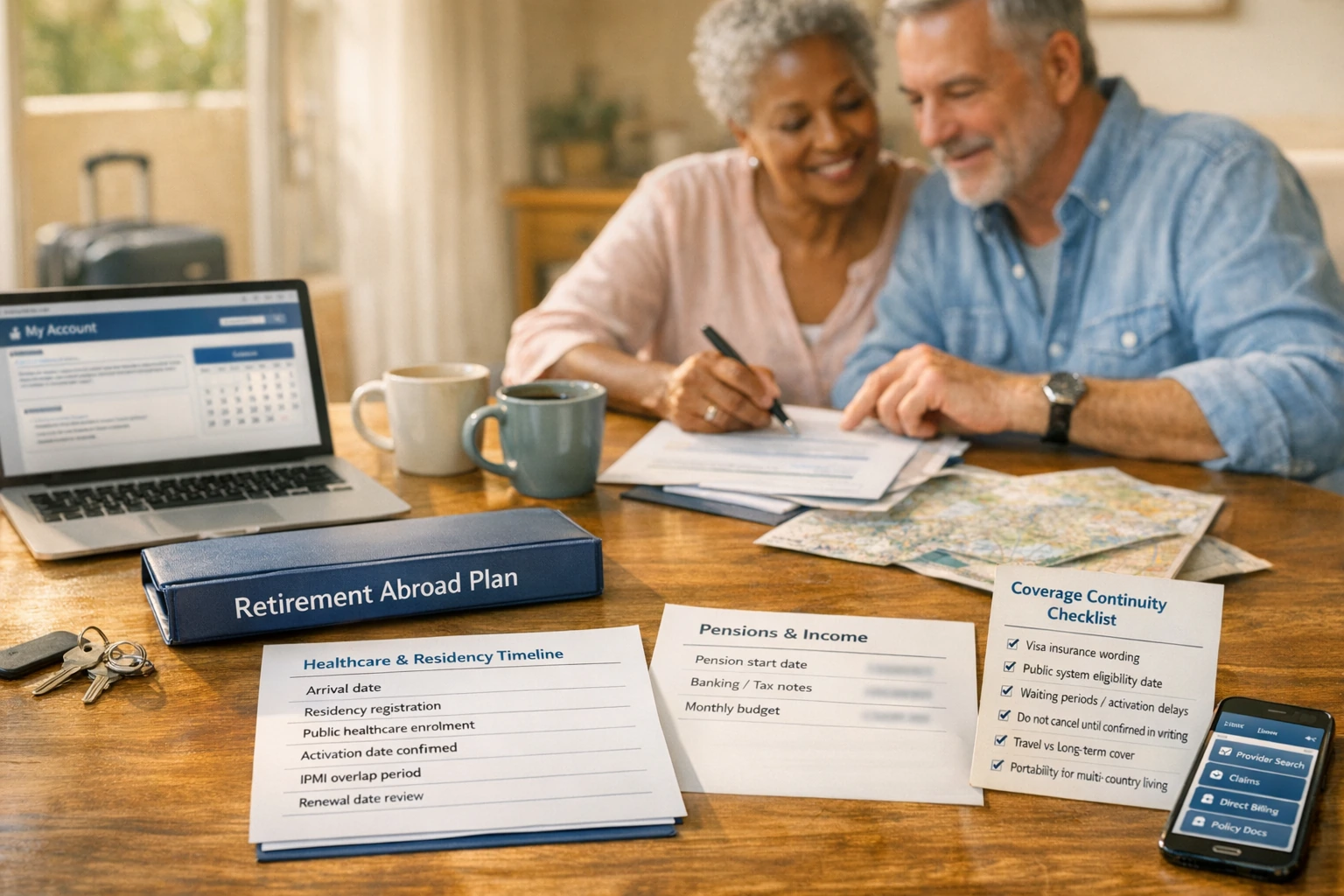

7. Checklist for retirement planning

Use this as a master list for your multi-year plan. Adjust the timeline based on your move date and your visa/residency route.

- Residency and visas: Confirm requirements (income, medical cover, documents). Apply early.

- Local healthcare registration: Learn how to enrol, what documents you’ll need, and the expected activation timeline.

- Existing insurance review: Don’t cancel until replacement cover is active and confirmed in writing.

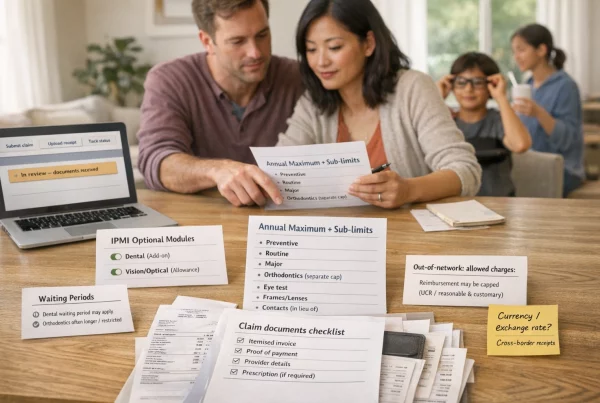

- Plan IPMI cover (if needed): Choose area of cover, deductible/excess, and benefits for your lifestyle and budget.

- Medical records: Gather and (if needed) translate records, prescriptions, and specialist letters.

- Budgeting: Plan for premium increases and likely out-of-pocket costs (deductibles/excesses, co-payments, excluded services).

- Provider research: Identify local clinics/hospitals, and confirm network/direct billing options where applicable.

- Move-day plan: Make sure you have cover from day one (arrival date) and emergency contacts saved.

- Renewal mechanics: How is the premium calculated at renewal? Can benefits/terms change, and how much notice is given?

- Age-related pricing: Do you use age bands? When do step-up increases apply?

- Coverage area: Which countries are included/excluded? Is your “home country” covered and, if so, for how long each year?

- Network / direct billing: Which providers can bill directly where you live? What happens if you go out of network?

- Pre-existing conditions: What is covered, excluded, or subject to waiting periods/limits?

- Residence evidence: Do you need proof of residence for eligibility or claims?

- Cancellation & overlap: What notice is required, and how long should policies overlap to avoid gaps?

- Visa wording: Can you issue certificates that match visa requirements (and is the insurer authorised locally if required)?

8. Broker’s role

A specialist broker can help translate your situation (health history, mobility plans, budget constraints) into practical cover priorities. We compare policy wordings, flag fine-print pitfalls, and help you align plan design (deductibles/excesses, territory, modules) with what you can sustain over time.

Brokers can also support you at renewal — explaining options, managing timings, and helping you avoid gaps when switching policies. However, insurers ultimately make underwriting and pricing decisions, and market-wide medical inflation affects most plans.

- Bring your expected residency timeline, travel pattern, and budget range.

- Share what you genuinely value (speed, private provider choice, portability, chronic care, predictable costs).

- Use your broker for paperwork and comparisons — but verify key requirements (visa, public enrolment) with official sources.

Get Started

If you’re planning a move (or you’re already abroad), we can help you structure cover around your residency timeline and long-term budget. Visit our Individuals & Families page to explore options. If you already have cover and want a second opinion, see Already Covered (Review my existing policy).

Ready to apply? Get a Quote. For quick answers to common questions, visit our FAQ.

Helpful background reading: Understanding International Health Insurance (IPMI) and Renewal strategies (managing premium increases).

Points to verify

Before relying on any “typical” pathway, confirm these points for your country, visa, and insurer:

- Public healthcare eligibility: residency requirements, waiting periods, and enrolment steps.

- Pension eligibility: contribution years needed, treaty/totalisation rules, and taxation of foreign pensions.

- Residency definition: how “habitual residence” is assessed (time in country, ties, registration, tax status).

- Visa insurance proof: required wording/benefits (and whether the insurer must be authorised locally).

- Renewal mechanics: age bands, premium calculation, and how plan changes work at renewal.

- Chronic/pre-existing conditions: underwriting approach, waiting periods, exclusions, limits, and any authorisation rules.

- Portability limits: time restrictions in certain countries and requirements to notify residence changes.

- Coordination with public cover: whether private claims are reduced by public benefits, and how billing works.

Being clear on these points early helps prevent unpleasant surprises when you’re already abroad and trying to access care.

Disclaimer

This article is for general information only and does not constitute financial, tax, pension, medical, legal, or insurance advice. Eligibility for public healthcare or pensions depends on country-specific rules, residency status, contribution history, and treaties. Insurance premiums, underwriting outcomes, and claim payments depend on insurer terms and market conditions. Always verify requirements with official authorities and qualified advisers, and review your policy documents carefully.