Underwriting is the part of international health insurance that determines what your policy means in practice: what’s covered, what’s excluded, and how much you pay. If you’re moving countries — for example, relocating to Europe (including Switzerland) or moving from Europe to the US — underwriting is also where questions about “portability” and continuity typically arise.

When you’re relocating, it’s easy to treat health insurance as a tick-box task. But underwriting is what determines how your cover will work when you actually need treatment. It’s the insurer’s process for assessing risk and setting the terms of your policy (for example: standard terms, a premium loading, specific exclusions, or in some cases, a decline).[1]

With international private medical insurance (IPMI), underwriting usually takes place at the outset and the policy then renews in line with the insurer’s renewal terms. That’s why the way you apply — and what you disclose — matters more than most people expect. In many jurisdictions, the information you provide is “material” to the insurer’s decision. If you don’t disclose something that would have affected the terms offered, it can have consequences at claim stage.[2][3]

This guide explains IPMI underwriting in plain English — in particular the difference between full medical underwriting and moratorium underwriting, how insurers approach pre-existing conditions, and what you can do to keep the process clear and predictable.

Note: Terms vary by insurer and jurisdiction. Where something depends on the policy wording, we flag it and include it in Points to verify.

- Underwriting sets your terms: price, exclusions and how pre-existing conditions are treated.[1]

- Full medical underwriting (FMU): you complete a medical questionnaire; the insurer confirms terms upfront (clearer outcomes, but more disclosure work).[4]

- Moratorium underwriting: fewer medical questions; pre-existing conditions are excluded for a defined “clean” period (commonly 24 months).[4]

- “Pre-existing condition” varies by policy: often something you had symptoms of, received treatment for, or were diagnosed with before cover started.[2]

- Waiting periods are common: some benefits only become available after a set period (for certain types of treatment).[5]

- Disclosure is critical: non-disclosure or misrepresentation can affect claims and, in some cases, policy validity (depending on law and wording).[3]

- Moving country can change things: IPMI can be designed to follow you across borders, but residency rules and area of cover still apply — check before you cancel or let an existing policy lapse.

Why underwriting matters

Underwriting is the insurer’s process for assessing risk and deciding the terms on which they’re prepared to offer cover. In health insurance, that usually means reviewing your medical history and other relevant risk factors before the policy is issued (or before it’s issued on standard terms).[1]

Underwriting matters in IPMI because you’re often buying cover you want to keep through life changes: a new country, a new job, a growing family, or a new diagnosis. If you don’t understand underwriting at the outset, you can end up with avoidable gaps or unpleasant surprises later on.

Underwriting can result in standard terms, premium loadings, exclusions (temporary or permanent), and sometimes a decline. Those terms form the basis for how claims are assessed.

Many people consider IPMI because their life spans more than one country — for example, relocating to Europe (including Switzerland) and later spending time in the US, or moving from Europe to the US. Portability can be an advantage, but residency and geographical rules still apply and should be checked.

What you disclose during underwriting can affect how future claims are handled. Depending on the jurisdiction and policy terms, non-disclosure can lead to reduced benefits, a disputed claim, or (in serious cases) the insurer treating the policy as void.[3]

Underwriting isn’t just “paperwork”. It’s the insurer turning your health history into a contract. Once you see it that way, the right questions become clearer: what counts as pre-existing, what’s excluded, what waiting periods apply, and what happens if you move.

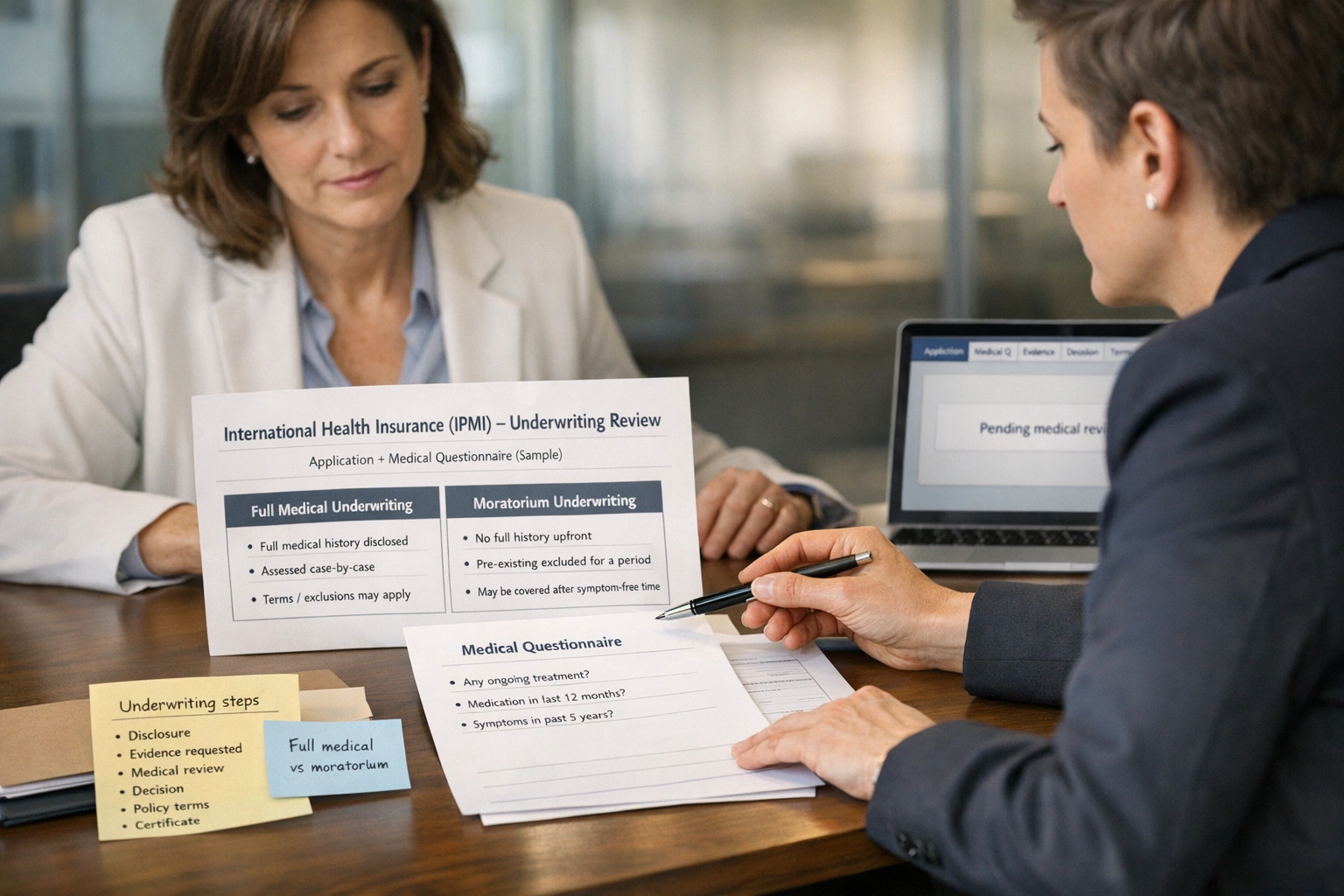

Types of underwriting (full medical vs moratorium)

IPMI is commonly offered on two main underwriting approaches: full medical underwriting and moratorium underwriting. Both manage risk, but they do so in different ways — with different trade-offs in speed, certainty, and how pre-existing conditions are treated.[4]

Text-based underwriting pathway diagram (simplified)

Start → Choose underwriting route → Insurer sets terms

-

Route A: Full medical underwriting (FMU)

- You complete a detailed medical questionnaire.

- The insurer reviews what you’ve disclosed and may request supporting evidence.

- Outcome: standard terms, a premium loading, a specific exclusion (or exclusions), or a decline.[1]

- Benefit: you will usually know your terms before cover starts.

-

Route B: Moratorium underwriting

- You answer limited questions (often without completing a full health questionnaire).

- Pre-existing conditions are excluded for a defined “moratorium” period (often 24 months free of symptoms and treatment).[4]

- After the “clean” period, some conditions may become eligible for cover (subject to the policy wording).

- Benefit: quicker set-up; the premium and terms are driven by the insurer’s rules and plan design.

Some insurers also use “continued personal medical exclusions” (CPME) when you switch policies — meaning exclusions carry over. Availability varies.

Full medical underwriting (what it is, what it tends to suit)

Full medical underwriting means you declare your medical history through an insurer questionnaire (often for each person covered). The insurer uses that information to confirm the terms before the policy starts.[4]

- Why people choose it: clear terms from day one; particularly helpful if you want a known condition assessed explicitly.

- Common trade-off: more work upfront, and you may be asked for reports or letters (specialist notes, test results, and so on).

Moratorium underwriting (what it is, what it tends to suit)

Moratorium underwriting usually avoids a full medical questionnaire. Instead, the policy excludes pre-existing conditions for a defined period — commonly expressed as being symptom-free and treatment-free for a set time (often 24 months).[4]

- Why people choose it: speed and simplicity; it may suit applicants with little or no recent medical history.

- Common trade-off: less certainty upfront; you need to understand what the insurer counts as “treatment” and what may restart the moratorium period.

A decision framework (use with caution)

| Your situation | FMU may suit you if… | Moratorium may suit you if… | What to double-check |

|---|---|---|---|

| You want certainty | You want the terms confirmed in writing upfront (exclusions/loadings agreed before cover starts). | You’re comfortable with the moratorium approach and the “clean period” concept. | How the policy defines “pre-existing”, “symptoms” and “treatment”. |

| You have a medical history | You want the insurer to assess it and confirm, in writing, how it will be treated. | Your history is older/minor and you expect to meet the symptom-free and treatment-free requirement. | Whether some conditions can remain excluded under the moratorium wording. |

| You’re relocating soon | You can provide information promptly and have time for underwriting review. | You need cover to start quickly and can accept uncertainty around historical issues. | Geographical scope and residency rules (especially if moving to/from the US or Switzerland). |

This framework is deliberately cautious: underwriting rules vary by insurer, plan level and jurisdiction. Always check the policy wording and confirm specifics.

How insurers assess pre-existing conditions

A “pre-existing condition” generally means a health issue that existed before your cover start date. In many health insurance contexts, this includes conditions you were diagnosed with, received treatment for, or had symptoms of before cover began.[2]

In IPMI, insurers usually assess pre-existing conditions in two layers: (1) the policy definition (what counts), and (2) your medical history (how it applies to you). The same condition may be treated differently depending on severity, how recent it is, how stable it is, and whether ongoing treatment is expected.

What insurers typically consider

- Recency: how recently you had symptoms, changes in medication, investigations/tests, or treatment.

- Stability: whether the condition is controlled and stable, versus active or deteriorating.

- Complexity: whether conditions are linked (e.g., hypertension + diabetes + kidney issues).

- Expected care: the likelihood of follow-up, monitoring, or future interventions.

Waiting periods vs moratorium (don’t confuse them)

Waiting periods are common in insurance: certain benefits only become available after a set time (for example, some employer benefits start after 30–90 days, and some benefits such as maternity can have longer waiting periods).[5]

Moratorium underwriting is a separate mechanism applied to pre-existing conditions: the condition remains excluded until you meet the policy’s “clean period” requirements (often expressed as being symptom-free and treatment-free for a defined period).[4]

Under moratorium underwriting, the definition of “treatment” can be decisive. Under some policies, medication, follow-up appointments or tests may count as treatment and restart the clean period. Always ask how the insurer treats monitoring, routine reviews and maintenance medication for stable conditions.

Illustrative examples (not guarantees; terms vary by insurer)

FMU: the insurer may offer standard terms, apply a loading, or apply an asthma-related exclusion depending on severity and recent treatment.

Moratorium: asthma may be excluded until the clean period is met, but ongoing inhaler use may count as treatment and keep the exclusion in place.

Illustrative only. Always check the policy definition and the insurer’s decision.

FMU: the insurer may exclude the knee (and potentially related complications) or apply a loading depending on recovery, function and expected future risk.

Moratorium: knee-related claims are likely excluded until the moratorium period is satisfied; follow-up physiotherapy may restart the clean period.

Not a prediction — simply a common underwriting approach.

If symptoms begin after the policy starts and there were no prior symptoms or treatment, the issue may not be treated as “pre-existing”. However, claim decisions depend on the policy definition and what’s recorded in medical notes.

If there was earlier investigation or documented symptoms, insurers may assess it differently.

Non-disclosure risk (why insurers care)

Underwriting relies on accurate information. Many jurisdictions have consumer protection rules around unfair practices, while also allowing insurers to investigate misrepresentation and material non-disclosure where that information would have affected the underwriting decision.[3]

The practical takeaway is simple: disclose fully and clearly. Where something is unclear, add context and dates. If helpful, include a short note and supporting documentation so the underwriter has the full picture.

Impact on premiums and exclusions

Underwriting outcomes usually affect your policy in two ways: what you pay and what’s covered. Under full medical underwriting, the insurer can apply individual terms based on what you’ve disclosed (for example, a premium loading or specific exclusions). Under moratorium underwriting, pre-existing conditions are typically excluded during the moratorium period.[4]

Common underwriting outcomes (high level)

- Standard terms: no additional premium and no special exclusions beyond the standard policy wording.

- Premium loading: the insurer increases the premium to reflect the risk profile (often linked to medical history or other risk factors).

- Exclusion: the insurer excludes cover for a named condition (or a body system). This may be permanent or time-limited, depending on the terms.

- Decline: the insurer decides the risk is outside appetite for that plan (or, in some cases, any plan they offer).

How exclusions typically work

| Type | How it usually works | What you should check |

|---|---|---|

| Specific exclusion (FMU) | A named condition is excluded from cover (e.g., “asthma”, “lumbar spine”, “complications of diabetes”). | Whether related complications are excluded as well, and how the policy defines “related”. |

| Moratorium exclusion | Pre-existing conditions are excluded until you meet the clean period requirement (commonly symptom-free/treatment-free for a set time).[4] | What counts as symptoms/treatment; what restarts the clean period; whether any conditions never become eligible. |

| Benefit waiting period | Some benefits are not available until a set period has passed (policy-specific).[5] | Which benefits have waiting periods (maternity, dental, certain therapies) and whether it varies by country. |

What changes when the US is included in your area of cover

Many IPMI plans allow you to choose an area of cover (for example, worldwide excluding the US versus worldwide including the US). Including the US can significantly increase the premium because healthcare costs are generally higher. The exact impact depends on the insurer’s pricing, your deductible/excess, and the benefit design.

We’ve avoided quoting “typical” price differences because the range is wide and highly dependent on the insurer and your circumstances. Ask for like-for-like quotes to compare properly.

Tips for applicants with medical history

If you have any medical history — even if it feels minor — the aim is to make underwriting as predictable as possible. Predictability comes from clear, consistent information: dates, diagnoses, stability, current medication, and supporting documents where needed.

Checklist: preparing medical information (documents + how to disclose)

- GP / primary care summary showing diagnoses, current medication, and whether conditions are stable/controlled.

- Specialist letters for any ongoing conditions (cardiology, endocrinology, respiratory, etc.).

- Hospital discharge summaries and operative notes for surgery or admissions.

- Test results (blood tests, imaging, ECGs, scans) with dates.

- Medication list (name, dose, frequency) including start dates where possible.

- A simple timeline for each condition: onset → diagnosis → treatment → last symptoms → last treatment.

- Disclosure approach: answer the insurer’s questions precisely; where something doesn’t fit neatly, add a brief note and attach evidence.

- Consistency check: ensure your disclosure aligns with your medical notes (especially dates and medication history).

What to do if you’re unsure whether something “counts”

If you’re unsure whether something is relevant, it’s usually safer to disclose it with context. A short note such as “single episode, resolved; no medication since; no recurrence” can help the underwriter interpret it correctly.

Underwriting-focused questions to ask (broker or insurer)

- Which underwriting approach applies (FMU, moratorium, or something else)?[4]

- How does the policy define “pre-existing condition”, and is there a look-back period?[2]

- Under moratorium: what counts as “treatment” or “symptoms”, and what restarts the clean period?

- Are exclusions narrow or broad (condition only vs related conditions/body systems)?

- Which benefits have waiting periods, and how long are they?[5]

- How does renewal work: are terms typically the same at renewal, and when could terms change?

- If you move country, does cover remain in force and what changes (area of cover, provider networks, currency, tax rules)?

Mobility tip: don’t cancel too early

If you already have cover (particularly if you’ve completed waiting periods or have established exclusions you understand), it’s often worth checking whether any continuity options or switching arrangements apply before you cancel or allow the policy to lapse. This is especially relevant when relocating to Europe/Switzerland or moving from Europe to the US and you want to maintain continuity.

Underwriting decisions are made by the insurer; a broker cannot guarantee acceptance or the removal of exclusions. Our role is to help you compare options and submit a complete, accurate application.

When to seek broker guidance

Underwriting is often straightforward if you have little or no medical history and your residency and area of cover are simple. It becomes more complex if you have long-term conditions, incomplete medical records, multiple countries in scope, or a tight timetable (for example, an imminent move).

Situations where broker support typically adds value

- You have a medical history and want clarity on whether FMU or moratorium is more appropriate.

- You’re moving across regions (e.g., Europe/Switzerland ↔ US) and need help setting the right area of cover and continuity.

- You’re switching insurers and want to understand how exclusions and moratorium terms may carry across.

- You’re covering a family and want to avoid inconsistent disclosure across different insured persons.

- You want a compliant, evidence-led approach that reduces the risk of disputes at claim stage.

We can help you structure the cover, compare underwriting approaches, and support accurate disclosure with appropriate documentation. We can’t control the insurer’s underwriting decision, guarantee acceptance, or promise that exclusions will be removed.

If you’re exploring international cover for yourself or your family, our service pages may help: see Individuals & Families, and if you’re already insured, see Already Covered.

Summary checklist

- Choose your underwriting approach: full medical vs moratorium — understand the trade-offs.[4]

- Define “pre-existing” for your policy: confirm the insurer’s wording and any look-back period.[2]

- Prepare documentation: GP summary, specialist letters, tests, and a timeline (especially for long-term conditions).

- Ask about waiting periods: which benefits have them, and for how long.[5]

- Check geography: if you need US cover now (or may later), confirm area of cover, eligibility rules, and the cost impact.

- Don’t cancel too early: check whether continuity options or switching terms apply before cancelling or allowing an existing policy to lapse.

- Confirm renewal terms: how renewals work and whether changes to cover trigger fresh underwriting.

- Get key terms in writing: exclusions, loadings, moratorium terms, and any special endorsements.

If you’re comparing international health insurance options for yourself or your family, start here: Individuals & Families. When you’re ready, you can request a quote, and for common questions see our FAQ. If you already have a policy and are considering changes, review Already Covered before you cancel or allow your policy to lapse.

Further reading: Choosing the Right Insurer for International Health Insurance and Understanding International Health Insurance (IPMI).

Points to verify

- Definition of “pre-existing condition”: definitions, look-back periods and wording vary by insurer and jurisdiction.[2]

- Moratorium clean period: the duration (often 24 months) and what restarts it (symptoms, tests, medication) varies by insurer.[4]

- Waiting periods: which benefits have waiting periods, and for how long, depends on the plan design.[5]

- Scope of exclusions: whether exclusions are narrow (single condition) or broad (related conditions/body systems) depends on the wording.

- Renewal and changes: confirm whether cover renews on the same terms, and whether upgrades or adding benefits triggers fresh underwriting.

- Area of cover and residency rules: confirm how cover works if you relocate (e.g., Europe/Switzerland ↔ US), and whether the policy remains valid.

- Disclosure rules and consequences: how misrepresentation/non-disclosure is handled varies by jurisdiction and policy terms.[3]

- Local plan limitations: local plans may be designed mainly for one country; confirm portability, emergency cover abroad, and any limits on time spent outside the home country.