Dental and vision costs are often predictable — and that’s exactly why they can feel confusing within international private medical insurance (IPMI).

Many IPMI plans focus mainly on higher-cost medical expenses, while dental insurance and optical (vision) benefits (where available) are often offered as optional modules with their own rules.

Those rules can include annual maximums, sub-limits, dental waiting periods, frequency limits, network restrictions, and reimbursement rules that don’t always mirror your core inpatient/outpatient cover.

This guide explains how IPMI dental and vision benefits are commonly structured, what to look out for, and how expatriate families can decide what’s worth adding — without assuming any benefit is universal and without giving treatment advice.

- Dental and vision are often optional: Many IPMI policies treat them as add-ons or low-limit “extras”, and the detail varies widely by insurer and plan design.

- Expect caps: Dental/optical benefits commonly use annual maximums plus sub-limits and frequency rules, so they’re often a budgeting tool rather than open-ended cover.

- Waiting periods can apply: Dental waiting periods (and longer orthodontic waiting periods, where offered) are common levers used to manage predictable claiming patterns.[7]

- Sub-limits drive outcomes: The headline “dental benefit” matters less than the internal sub-limits (preventive vs major, per-procedure caps, orthodontics rules).[12]

- Out-of-network shortfalls are real: Reimbursement may be capped by “reasonable & customary”/UCR-style allowances, leaving you to pay the difference if fees are high.[13][14]

- Good admin reduces friction: Itemised invoices, proof of payment and clear receipts (especially abroad) are often what prevents delays.[15]

- Your decision is usually lifestyle and budgeting maths: Where you live, how often you move, and whether children have predictable glasses costs or dental utilisation often matters more than brochure wording.

Overview of dental and vision benefits

Dental and vision benefits within IPMI are often designed differently from core medical benefits. In many markets, they are regular, predictable costs, which means insurers commonly manage them with tighter limits and clearer eligibility rules.

The key point to bear in mind (because it prevents most misunderstandings) is straightforward: dental and vision cover is often optional and varies widely by insurer, plan tier and country. Even when a plan says “dental included”, it may be limited to emergency dental only, or it may be a small allowance rather than broad dental insurance.

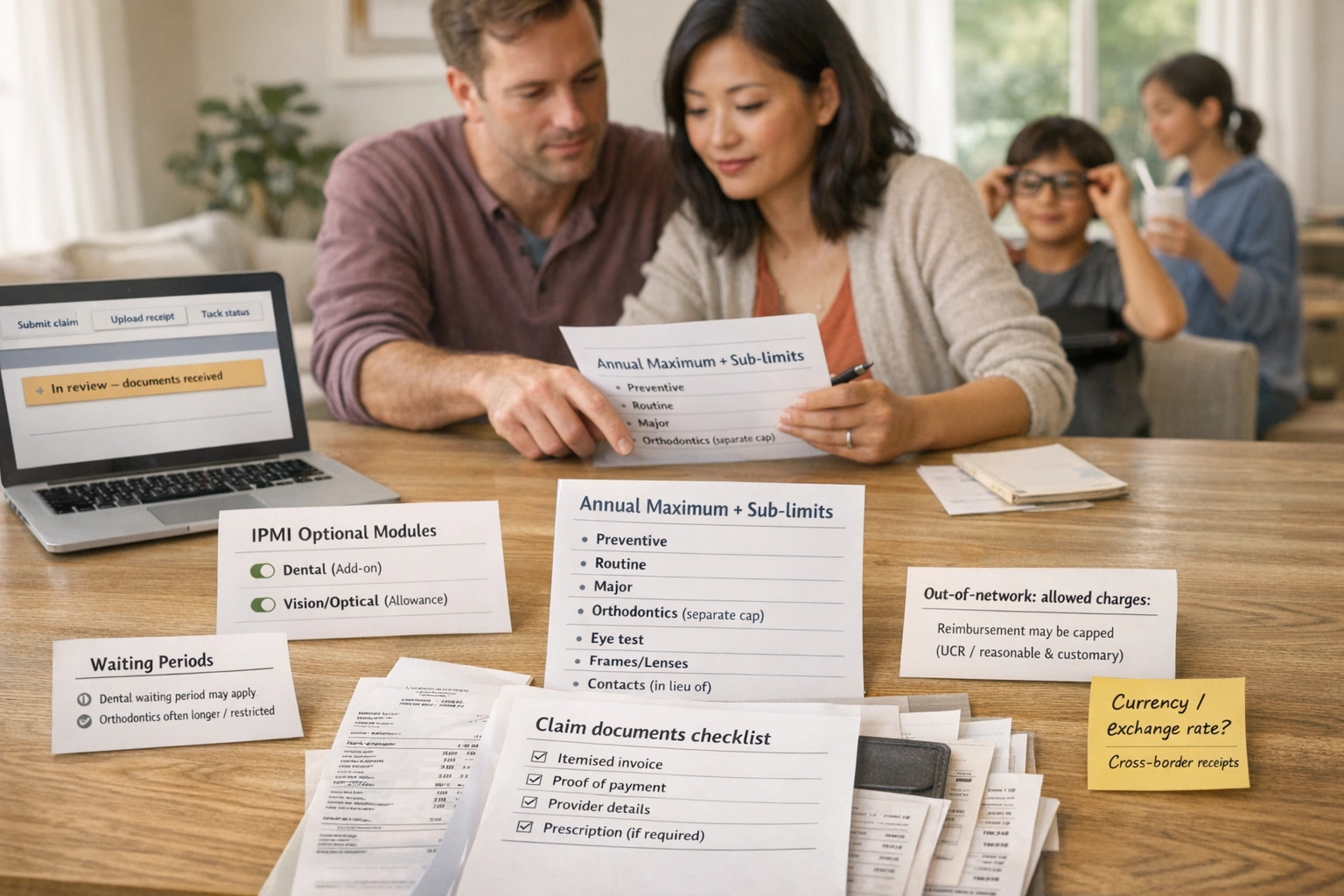

- Dental benefit: A defined set of dental services reimbursable by the policy, usually subject to an annual maximum and/or sub-limits.

- Routine vs major dental: In benefits design, “routine/basic” commonly covers diagnostic and preventive care plus basic restorative work; “major” commonly covers more complex restorative care. The exact boundary varies by policy and insurer.[3]

- Preventive dental: Care intended to maintain oral health and identify problems early (for example, routine examinations/assessments). NHS guidance notes that a dental check-up examines teeth, gums and mouth and reviews any issues since your last visit; the content can vary by provider and country.[1]

- Waiting period: A period during which a benefit is not payable (or is restricted) even though your policy is in force. Waiting period concepts are recognised in consumer insurance glossaries.[7]

- Sub-limit: A smaller cap within a broader benefit (for example, an annual dental maximum with a lower cap inside it for a specific procedure). The Financial Ombudsman Service explains that policies can have a main limit and additional sub-limits that restrict certain costs.[12]

- Annual maximum (annual limit): A cap on what the plan pays in a year for a benefit section (often used in dental; sometimes used in optical). HealthCare.gov defines an annual limit as a cap on benefits in a year.[10]

- Co-insurance (coinsurance): The percentage share of eligible costs you pay after any excess/deductible is applied. HealthCare.gov defines coinsurance as your share of costs expressed as a percentage.[9]

- Excess (deductible): The amount you pay towards eligible costs before the plan starts to pay. HealthCare.gov defines a deductible in these terms (terminology varies by market).[8]

- Network vs out-of-network: A “network” is a set of providers with insurer arrangements; “out-of-network” means no arrangement and can mean you pay up front and claim back, with different reimbursement rules. The NAIC uniform glossary defines preferred provider and explains UCR-style approaches used to determine allowed amounts.[13]

- “Reasonable & customary” / UCR: A reimbursement approach where eligible charges can be capped based on typical fees in a region. The NAIC glossary defines UCR, and insurers may refer to “reasonable and customary” amounts in member guidance.[13][14]

- Orthodontics: In benefits design, orthodontics is frequently treated as a separate category and may be excluded, capped separately, or subject to additional eligibility rules. Dental plan examples often show a separate orthodontic maximum (sometimes lifetime-style).[3]

- Optical / vision benefit: A benefit that contributes towards eye tests and/or corrective eyewear (often through fixed allowances and frequency rules rather than open-ended reimbursement).

Tip: keep this glossary open while reading your benefits schedule. Many “surprises” are simply the policy definitions doing what they say.

Why dental and vision benefits are structured differently

Insurers tend to treat core medical cover as protection against high-cost events. Dental and vision, by contrast, are often used regularly and predictably, which can encourage a “take out cover and claim straight away” pattern if there were no restrictions.

That is why many dental and optical benefits (where offered) rely on annual maximums, sub-limits, waiting periods, frequency rules and reimbursement schedules. These controls do not necessarily mean the cover is “bad”; they usually mean it is designed as a managed, capped benefit.

What’s a realistic goal for dental/vision cover in IPMI?

A practical way to evaluate IPMI dental and vision is to decide what you want the cover to do: reduce routine costs you pay yourself, contribute towards higher-cost work, or simply add more predictability for a family.

We deliberately do not discuss treatment choices in this guide. The focus is solely on insurance mechanics, decision-making and admin.

Common structures (add-ons vs embedded)

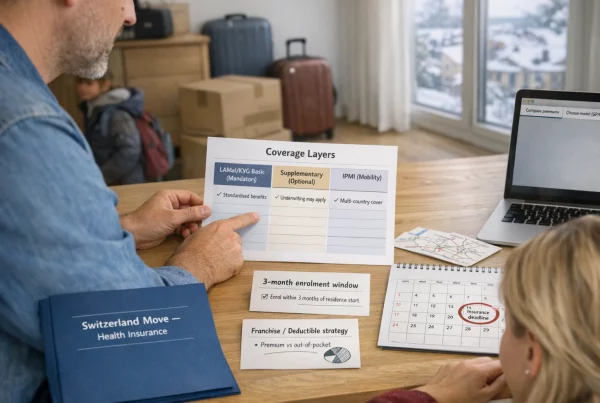

In the IPMI market, dental insurance and optical (vision) benefits typically appear in one of three structures. Identifying which structure you have is step one, because it determines how limits and claims work in practice.

You buy a core IPMI plan and optionally add dental and/or optical benefits. The module usually has its own annual maximum, sub-limits and sometimes a separate waiting period.

A good fit if you want predictable contributions to routine spending and you’re comfortable working within caps.

A plan may include a small amount of dental or optical cover in the core policy (for example, emergency dental only, or a modest optical allowance). It can reduce smaller costs, but it is rarely comprehensive.

Risk: you may assume “included” means broad cover. Always check the benefit definition and sub-limits.

Some expatriate households pair IPMI with a local dental plan (and/or an optical plan or employer benefit). This can be cost-effective in one country, but can reduce portability if you move.

Expect extra admin: two policies, two claims routes, two networks (and sometimes two languages).

Common market patterns: typical dental/vision benefit structures and sub-limits

The table below describes common market patterns — not insurer-specific commitments. Use it to recognise the “shape” of a benefit and pinpoint what you must verify in your policy wording.

| Benefit type | Common structure in IPMI | Typical limit pattern (how it’s capped) | Cost-sharing pattern (how you pay) | Where surprises happen |

|---|---|---|---|---|

| Preventive dental | Often included within a dental module; sometimes partially embedded | Annual maximum and/or frequency rule; sometimes a separate preventive sub-limit | May be reimbursed at a higher percentage than major dental, or paid up to a schedule/allowance | “Preventive” definitions vary. If you exceed frequency limits, reimbursement may reduce or stop. |

| Routine/basic dental | Usually inside the dental module | Shares the annual maximum; may have per-procedure caps | Co-insurance is common; sometimes an excess/deductible applies[8][9] | Category mapping: the same procedure can be “basic” in one plan and “major” in another. |

| Major dental | Usually inside the dental module, often with tighter controls | Tighter sub-limits and sometimes waiting periods; may be capped by an allowed-charge schedule | Higher co-insurance is more common; out-of-network shortfalls are possible if capped by UCR/reasonable & customary[13][14] | “Covered” does not always mean “fully paid”: sub-limits plus allowed-charge caps can leave a balance. |

| Orthodontic coverage | Often excluded, or offered with strict conditions | Commonly a separate cap (sometimes lifetime-style); waiting periods and age rules can apply[3] | Co-insurance is typical where offered | Assuming orthodontics is included is a common mistake. Always verify eligibility and caps. |

| Emergency dental | Sometimes separated from routine dental; occasionally embedded | May have its own limit or be handled under outpatient/emergency rules | Varies widely; reimbursement vs direct billing depends on provider arrangements | Definitions matter (“accident”, “trauma”, “acute pain”) and can differ by insurer wording. |

| Eye test / sight test | Optical benefit or small embedded allowance | Fixed allowance and/or frequency rule | Often reimbursed up to a maximum; documentation requirements are common | If your receipt is not itemised or lacks provider details, claims can be delayed.[15] |

| Glasses cover (frames/lenses) | Optical allowance model | Annual or multi-year allowance; sometimes separate caps for frames vs lenses | You pay anything above the allowance | Allowance ≠ “free glasses”. Higher-priced retailers can leave larger gaps. |

| Contact lenses | Often “in lieu of glasses” within the optical allowance | Allowance + frequency rules | Any balance above the allowance is your cost | Some plans require a prescription/report; many require proof of payment.[15] |

| Refractive surgery | Often excluded or tightly limited | If covered, usually strict criteria and low caps; pre-authorisation may apply[13] | Varies; often not treated as routine optical | Don’t assume it sits under “vision”. Verify separately in the wording. |

The table is intentionally non-numeric. Limits vary widely by insurer, plan tier and geography — treat your benefits schedule as the source of truth.

Waiting periods and sub-limits

If you want to avoid surprises, focus on five areas of policy mechanics: waiting periods, annual maximums, sub-limits, cost-sharing, and how “eligible charges” (the insurer’s allowed amount) are calculated — especially out-of-network.

Waiting periods: what they mean in practice

A waiting period is a period when cover exists but is not yet payable (or is only payable in a limited way).[7] In dental/vision modules, waiting periods are often used to manage immediate claiming behaviour on predictable benefits.

Typical patterns you may see (these are patterns, not guarantees):

- No or short waiting period for preventive dental or basic optical allowances.

- Longer waiting periods for major dental services and for orthodontic cover (where available).

- Staged benefits: some plans pay a lower percentage in the first year and increase later (varies by insurer and market).

Waiting periods vary materially by insurer and policy. Always verify the exact start date, the scope of the restriction, and what evidence may be required.

Annual maximums: the “budget ceiling”

Annual limits are caps on what a plan will pay in a year for a benefit section.[10] Dental plan designs often use annual maximums as a core control and may also use separate orthodontic caps in example designs.[3]

For expatriate families, the annual maximum question is very practical. You should ask:

- Is the annual maximum per person or shared across the family?

- Does preventive dental count towards the annual maximum, or is it treated separately?

- If you reach the maximum, does the benefit stop entirely for the remainder of the policy year?

Sub-limits and frequency rules: the hidden constraints

Sub-limits are caps within caps. The Financial Ombudsman Service describes sub-limits as restrictions that cap certain costs even when a broader limit exists.[12]

In dental and optical benefits, sub-limits and frequency rules often appear as:

- Maximum payable for a specific procedure category (for example, a lower cap for major restorative work).

- Frequency rules (for example, one eye test per year, frames once every 24 months).

- “In lieu of” rules (for example, claim contacts or glasses in one benefit period).

- Separate orthodontic caps (where offered) and eligibility restrictions (age rules, covered appliances, etc.).

Cost-sharing: excess/deductible and co-insurance

Dental and optical benefits often include cost-sharing, sometimes even where your medical cover feels more generous. Key concepts:

- Excess/deductible: what you pay before the plan starts paying eligible costs.[8]

- Co-insurance: your percentage share of eligible costs after the excess/deductible.[9]

- Out-of-pocket maximum: in some insurance contexts, the most you could pay for covered services in a benefit year (definitions and applicability vary by plan).[11]

A common retention-stage mistake is to assume that optional dental/optical modules follow the same cost-sharing protections as core medical benefits. In reality, optional modules can be capped independently and may have different cost-sharing arrangements.

Eligible charges: “reasonable & customary” / UCR and out-of-network shortfalls

If you use an out-of-network dentist or optician, reimbursement may be based on an “allowed amount” rather than what you were charged. The NAIC uniform glossary defines UCR (usual, customary and reasonable) as an amount based on typical charges for similar services in a geographic area; it may be used to determine allowed amounts.[13]

Insurer member guidance can also frame this as “reasonable and customary” — where you may be responsible for the difference between provider charges and what the insurer considers reasonable.[14] This is one reason why a plan can “cover” a service while still leaving you with a meaningful balance to pay.

If your dentist or optician charges more than the insurer’s allowed amount, you may face two layers of costs you pay yourself: (1) your excess/co-insurance and (2) any gap between the provider’s fee and the allowed amount.

Claims mechanics (practical): network vs out-of-network, documents, pre-authorisation, timelines

While core IPMI hospital claims often rely on direct billing, dental and optical benefits frequently work on a reimbursement basis. The exact approach depends on the insurer and the provider network (if any) in your country.

Need dental/optical care ↓ Check your policy benefit table: • Is the benefit included or optional? • Are there waiting periods, sub-limits, or frequency rules? ↓ Choose a provider: • In-network (if applicable) → may simplify billing and/or reduce shortfalls • Out-of-network → usually pay first, then claim (allowed-charge caps may apply) ↓ Before higher-cost work: • Ask whether pre-authorisation is required (varies by insurer and service category) ↓ Collect documentation: • Itemised invoice + proof of payment + provider details • Any forms or supporting documents required by the insurer ↓ Submit via portal/app/email (per insurer instructions) ↓ Insurer assesses and pays eligible costs (less any excess/deductible, co-insurance, and any amount over allowed charges)

Documentation: what to keep (especially when abroad)

Claims handling often runs more smoothly when your paperwork is clear, complete and easy to match to the benefit definition. Consumer guidance on claiming (even in other insurance contexts) commonly stresses keeping receipts and copies of documents; Citizens Advice recommends including copies of relevant paperwork and keeping copies of originals in case the claim is queried or refused.[15]

- Itemised invoice (not just a card receipt), ideally with clear line items.

- Proof of payment (receipt, card confirmation, stamped invoice, depending on insurer requirements).

- Provider details (name, address; professional registration number where available).

- Date(s) of service and a service description that maps to the benefit category.

- For optical: prescription or eye test record if your policy requires it.

Pre-authorisation: less common than hospital care, but not impossible

Some insurers require pre-authorisation for certain higher-cost services, even within optional modules. The NAIC glossary defines preauthorisation (prior authorisation) and notes that it is not a promise that the plan will cover the cost.[13]

A safe admin approach is to separate two questions:

- Is pre-authorisation required for this category of dental/vision claim?

- If it is approved, what limits still apply (annual maximum, sub-limit, co-insurance, allowed-charge cap)?

Reimbursement timelines: what to expect (careful language)

Reimbursement timelines vary by insurer, country and the completeness of your documents. Smaller claims are not always faster if receipts are unclear or the insurer needs translation or clarification.

Avoid relying on assumptions like “this should be automatic”. If you need predictability, ask the insurer how they handle dental/optical reimbursement where you live and what documentation issues most commonly delay payment.

Common pitfalls (and why they happen)

- Assuming dental is included: dental and vision are often optional add-ons in IPMI.

- Confusing preventive vs major dental: dental benefits often categorise services; because definitions vary, reimbursement can differ even for seemingly similar work.[3]

- Missing sub-limits: sub-limits can cap specific items even when an annual maximum looks adequate.[12]

- Overlooking orthodontics rules: orthodontic cover is commonly excluded or capped separately; waiting periods and eligibility rules (where offered) are frequent surprises.[3]

- Not noticing dental waiting periods: you may have the module active but still be within a waiting restriction.[7]

- Provider coding/receipts issues: unclear invoices and missing proof of payment create unnecessary follow-up and delays, especially across languages and currencies.[15]

- Out-of-network charge caps: allowed-charge methods (UCR/reasonable & customary) can reduce reimbursement even if the service is eligible.[13][14]

The goal isn’t to memorise every rule. It’s to ensure you can answer three questions quickly: Is it included?, What are the caps?, and What do I need to submit?

Comparing local and international dental plans

Many expatriate families find themselves comparing three routes: (1) adding dental cover to IPMI, (2) buying a local dental plan, or (3) paying for routine care themselves and using insurance only for specific scenarios (if covered).

There is no universal “best” choice. But there is a practical way to compare options so you can see the trade-offs before you commit.

Start with your real-life pattern: stability, travel, and provider habits

Local plans can work well when you are settled in one country and will use providers in that system. International dental modules can be attractive when you expect to move, when you value single-policy admin, or when you want consistent reimbursements across locations (even if modest).

If you move countries often, portability can matter as much as the annual maximum. Not every “local” arrangement transfers smoothly.

Compare mechanics before premiums

When comparing a local dental plan vs an IPMI dental add-on, it often helps to compare these factors in order:

- Scope: preventive dental vs routine vs major, and whether orthodontic cover exists at all.

- Limits: annual maximums and sub-limits (and whether they are per person or shared).[10][12]

- Waiting periods: especially for major dental and orthodontics.[7]

- Cost-sharing: excess/deductible and co-insurance proportions.[8][9]

- Provider access: network depth and how out-of-network reimbursements are calculated (UCR/reasonable & customary).[13]

- Claims admin: language, documentation requirements, and how easy it is to submit and track claims.

Reimbursement reality: how to avoid “paper cover”

A common mistake when comparing policies is to look only at whether a service is “covered”. For capped benefits, the more useful comparison is:

- How much could reasonably be reimbursed in a year if you use preventive dental only?

- How much could be reimbursed in a year if you have a more expensive-than-usual dental year (within the caps)?

- How much might UCR/reasonable & customary rules reduce reimbursement if you use higher-charging providers?[13][14]

A family decision framework (admin-only, no clinical advice)

If you want a simple but practical approach, try this:

- Look back: Roughly total your household’s dental & optical spending over the last 12–24 months (even approximate numbers help).

- Look forward: Identify predictable admin events (relocation, a travel-heavy year, children starting school, changes in employment benefits).

- Define your goal: Do you want contributions to routine costs, protection against moderate expenses, or simply one policy and one claims workflow?

- Stress-test the caps: Compare annual maximums and sub-limits against costs where you live (without assuming claims approval).

- Verify friction points: waiting periods, network rules, reimbursement basis, and documentation requirements.

This approach keeps the decision anchored in budget and admin realities rather than brochure wording.

If you want to go deeper on how to evaluate insurers beyond benefit tables (service model, claims experience, underwriting style), see our guide: Choosing the Right Insurer for International Health Insurance: how to compare what actually matters.

Optics (glasses/contact lenses) benefits

Optical benefits are often simpler than dental on paper — and still easy to misunderstand in real life. Most optical benefits are built as allowances: contributions towards an eye test and/or eyewear, capped by annual or multi-year limits.

What optical benefits commonly cover (in benefit language)

Opticians’ services can include an eye test (sight test) and prescribing corrective eyewear. For context, the NHS notes that when you visit an optician for an eye test you’ll be examined by an optometrist/ophthalmic practitioner trained to recognise abnormalities and conditions.[5] The College of Optometrists describes the routine eye examination/sight test as including internal and external examinations and other checks necessary to detect signs of injury, disease or abnormality, within the legal framework of a sight test.[6]

Insurers generally don’t cover “optometry” in the abstract. They cover specific categories — typically:

- Eye test / sight test allowance (often once per year or per benefit period).

- Materials allowance for glasses cover (frames/lenses) and/or contact lenses, often with “in lieu of” rules.

Allowance logic: why “glasses cover” often means “contribution”

If you’ve ever used a health cash plan, the structure might feel familiar. MoneyHelper describes health cash plans as covering routine expenses (including dental and optical) up to a limit.[16]

Many optical benefits in IPMI behave similarly: there is a limit, a frequency rule, and documentation requirements. That makes the benefit useful for predictable costs — but it can also be disappointing if you expect full reimbursement.

Why optical benefits are high-frequency (context only)

The World Health Organization notes that a large number of people experience vision impairment due to refractive errors and that many could be helped with spectacles, including reading glasses for presbyopia.[17] This does not tell you what eyewear you need — it simply helps explain why insurers design optical benefits as predictable-use allowances.

Optical claims: what helps them go smoothly

Optical claims are often documentation-driven. In general insurance guidance, keeping receipts and supplying appropriate paperwork is a consistent theme; Citizens Advice recommends including copies of relevant documents and keeping copies in case of queries or refusal.[15]

- Itemised invoice showing the eye test fee vs frames vs lenses vs contacts.

- Proof of payment.

- Prescription or eye test record if required by the policy wording.

- Provider details (especially important when claiming cross-border).

- Translation/supporting notes if invoices are not in a language the insurer will accept (varies by insurer).

Always follow your insurer’s required format. If your submission route is portal/app, upload legible PDFs and keep your original documents.

If you often buy eyewear in more than one country (for example, your country of residence vs your home country), ask how the insurer handles currencies, exchange rates and allowed-charge limits.

Questions to ask insurers

You don’t need dozens of questions to reduce surprises. You need the right questions that force clarity on what is included, what is capped, and how reimbursement is calculated.

Use the checklists below with your insurer or broker. Where possible, ask for confirmation against the policy wording rather than informal summaries.

- Is dental cover embedded in the core IPMI, or is it an optional add-on? If optional, can it be added for the whole family and all ages?

- How does the policy define preventive, routine/basic, and major dental? (Ask for the definitions, not just the labels.)[3]

- What is the dental annual maximum, and is it per person or shared across the family?[10]

- Do preventive dental claims count towards the annual maximum, or are they treated differently?

- What sub-limits exist inside the dental benefit (per procedure, per category, or per visit)?[12]

- Are there dental waiting periods? If yes, do they differ for preventive dental vs major dental?[7]

- Is orthodontic cover included, optional, or excluded? If included, is it capped separately and are there eligibility rules?[3]

- Does reimbursement use an allowed-charge approach (UCR/reasonable & customary), and how is it determined in your country?[13][14]

- Is optical a standalone add-on or embedded? If embedded, is it eye test-only or eye test plus materials?

- What exactly counts as an “optical benefit”: eye test, frames, lenses, contact lenses?

- Is it an allowance (fixed contribution) or a reimbursement percentage? If allowance, does it differ for frames vs lenses?

- What are the frequency rules (how often can you claim for an eye test, glasses, contacts)?

- Are contacts covered in lieu of glasses, or can both be claimed in the same benefit period?

- What documents are required (prescription, itemised invoice, proof of payment), and are digital receipts accepted?[15]

- Is there a dental/optical network in my country? What changes if I choose out-of-network?

- If out-of-network, is reimbursement capped by UCR/reasonable & customary or another allowed-charge method?[13][14]

- Are any dental/vision services subject to pre-authorisation? If approved, does that guarantee payment? (In general definitions, preauthorisation is not a promise of cover.)[13]

- What is the claim submission window (how long after treatment can I submit)?

- How should invoices be formatted, and what typically causes delays (translation, missing itemisation, missing proof of payment)?

- How will payments be made (bank transfer, cheque), and do I need to register bank details?

- How are currencies handled if treatment is paid in a different currency (exchange rate approach, bank fees)?

If you keep these answers in writing (or in annotated policy documents), you will usually avoid the most common “I didn’t realise…” issues at claim time.

Tips for keeping costs down

These tips focus on admin and cover optimisation — not treatment decisions. The aim is to reduce avoidable costs you pay yourself and preventable claim delays.

Use your benefits like a calendar and a budget

- Know your benefit year: annual maximums reset on a schedule; understand when yours resets and how that affects planning.

- Track utilisation: keep a simple record of what you’ve claimed so you don’t accidentally exceed sub-limits or frequency rules.

- Separate categories: if your plan has preventive vs major categories, confirm how items are classified before you assume reimbursement.

Reduce out-of-network shortfall risk

- Use network providers where it matters: if a network exists for dental/optical in your area, it can reduce shortfalls and simplify billing (varies by insurer).

- Ask for an estimate in writing before higher-cost work and compare it to your plan’s annual maximum and sub-limits.

- Understand allowed-charge rules: if your plan uses UCR/reasonable & customary, expect that higher-charging providers can leave a larger gap.[13][14]

Make claims “easy to assess”

Claims often slow down for predictable reasons: unclear invoices, missing proof of payment, or an incomplete submission. Citizens Advice guidance on claiming highlights the value of providing relevant paperwork and keeping copies in case of queries or refusal.[15]

- Request itemised invoices (especially abroad, where invoices can be brief by default).

- Keep proof of payment for reimbursement claims.

- Keep copies of everything: upload PDFs, store originals, and keep email/portal confirmations.

- Don’t wait: submit promptly so you’re within any claim submission deadline.

Use renewal as a structured review moment

Dental and optical needs change with life events: relocation, new schools, changes in employment benefits, and changes in travel patterns. Renewal is often the cleanest time to review whether optional modules still match your household’s expected usage.

For a broader framework on managing premium changes and reshaping cover without losing sight of the policy mechanics, see: Renewal strategies: managing premium increases and improving your cover.

Get Started

If you want help interpreting dental and optical benefits in real-world terms — including how annual maximums, sub-limits, waiting periods, and reimbursement rules typically interact — we can support you as a broker by translating policy language into clear decision points and a questions list tailored to your family.

Start here for Individuals & Families: https://big-brokers-health.com/individual-families/

For quick answers to common questions: https://big-brokers-health.com/faq/

Further reading:

Choosing the Right Insurer for International Health Insurance: how to compare what actually matters

Renewal strategies: managing premium increases and improving your cover

Points to verify

- Whether dental/vision is embedded or an add-on; eligibility rules

- Waiting periods for preventive, major dental, and orthodontics (if offered)

- Annual maximums and sub-limits (e.g., cleanings, fillings, crowns, orthodontics; frames/lenses/contacts)

- Cost-sharing (excess/deductible, co-insurance) and how reimbursements are calculated[8][9][10]

- Provider network rules and whether direct billing applies for dental/optical

- Whether “reasonable & customary” / UCR limits apply and how allowances are determined[13][14]

- Exclusions (cosmetic dentistry, pre-existing conditions rules if applicable, specialty services)

- Required documentation and time limits for claims[15]

If a concept varies materially by insurer/policy/country/provider, treat it as “verify before you rely on it”. For retention planning, the benefit is only as useful as the rules you can follow in practice.