If you’re researching expat insurance for chronic conditions, you’re probably not looking for sales promises. You want a realistic picture of how cover works in practice when you need regular specialist follow-up, high-cost medicines, or longer-term support while living abroad. International private medical insurance (IPMI) can help — but what happens in reality depends on underwriting, policy definitions, the provider network, prescription rules (formularies and prior authorisation), and the admin that sits behind the scenes. This guide sets out a decision framework, the questions to ask, and the planning steps that can reduce unpleasant surprises — without assuming any condition is “always covered”.

These are the areas most likely to affect access, cost, and stress levels once you’re abroad:

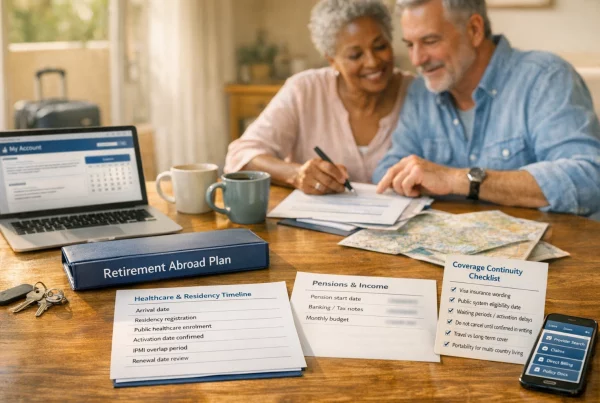

- Your current diagnoses, medication list (generic names, doses), and the last 12–24 months of key results are organised and easy to share.

- You understand whether your plan uses full medical underwriting or a moratorium approach for pre-existing conditions.[1]

- You’ve checked provider network access for the specialists you’re likely to need in your destination city.

- You’ve verified how the plan handles high-cost medicines: formulary status, prior authorisation, and any limits or sub-limits.[4]

- You understand the difference between direct billing and reimbursement, and when you may still need to pay up front.

- If longer-term support is relevant, you’ve clarified what “long-term care” means under the policy (if it’s included at all) and what may need separate arrangements.

- Cover varies: chronic conditions may be covered, excluded, or covered on special terms depending on underwriting, definitions, and your medical history.[1]

- Out-patient and prescriptions are pivotal: routine check-ups and medicines are where many budgets unravel — check benefits, sub-limits, and medication rules early.

- Formularies and prior authorisation are common: high-cost medicines often require approval and supporting documentation, and timing matters.[4]

- Networks change the experience: in-network specialists can make billing simpler; out-of-network care can mean paying up front and reimbursement limits based on “reasonable and customary” charges.

- Continuity of care is a process: bring a clear medical summary, translate essentials, and plan refills across borders to reduce the risk of gaps.[8]

- Long-term care is often limited: ongoing support (home care, assisted living) may be excluded or handled separately — treat this as something to verify, not an assumption.

- Use support: a broker can help you compare underwriting outcomes, interpret policy wording, and plan the admin steps before you relocate.

- Challenges of managing chronic conditions abroad

- What IPMI covers (in-patient, out-patient, medications)

- Underwriting and exclusions

- Accessing specialist care and networks

- Comparing local vs international solutions

- Continuity of care when relocating

- Checklist for patients and caregivers

- Broker support

Challenges of managing chronic conditions abroad

Chronic conditions are often manageable — but living abroad can add friction. You’re navigating a new healthcare system, often with different referral routes, pharmacy rules, and appointment availability. Insurance adds another layer: what matters isn’t just “do I have cover?” but “how does this policy handle my condition in practice?”

The most common pressure points for expats and families arranging chronic illness insurance usually fall into four areas: continuity (records and clinical handover), medications (availability, import rules, authorisation), networks (finding the right specialist who can bill your insurer), and policy mechanics (underwriting terms, exclusions, limits and sub-limits).

- Chronic condition: a long-term health issue that typically needs ongoing monitoring or treatment over months or years.

- Pre-existing condition: a health issue (symptoms, diagnosis, treatment, or medication) that existed before your policy start date; exact definitions vary by insurer and policy wording.

- Continuity of care: your care “joins up” across clinicians and locations — your records, medication history, and care plan follow you so decisions aren’t made in isolation.[7]

- Underwriting: the insurer’s process for assessing medical history and deciding what terms to offer (e.g., standard terms, exclusions, loadings).[1]

- Exclusion: a condition, treatment, or category of care the policy does not cover.[2]

- Medical loading: an additional premium charged due to higher perceived risk; it may be used instead of (or alongside) exclusions in some cases.[2]

- Moratorium: an underwriting approach where pre-existing conditions are excluded for a defined period; after a symptom-/treatment-free window, some conditions may become covered, depending on the policy rules.[1]

- Waiting period: a set time after the policy starts during which specific benefits aren’t payable (often used for categories such as maternity); it’s not the same as a moratorium.

- Pre-authorisation (prior approval): insurer approval needed before certain tests, procedures, admissions, or high-cost medicines; missing it can delay settlement and may affect claims handling.[4]

- Provider network: a list of hospitals, clinics, and clinicians with insurer arrangements; using the network can affect access to direct billing and negotiated rates.

- Formulary / specialty meds: the plan’s covered drug list; “specialty” often refers to higher-cost medicines that may require additional checks or authorisation.[4]

- Direct billing vs reimbursement: direct billing means the provider bills the insurer (you may still pay any excess/deductible and/or co-payment); reimbursement means you pay first, then claim back.

- Long-term care: ongoing help with daily living or extended support needs (e.g., home care, assisted living). Many medical plans limit or exclude this, or deal with it through separate arrangements.

Why “routine” care can become complicated abroad

In many countries, the route into specialist care is different from what you’re used to. Some systems rely heavily on referrals, others allow direct booking, and billing formats vary widely. Even where the clinical care is excellent, the admin — estimates, approvals, itemised invoices and translations — can feel like an extra part-time job.

Medication logistics can be the hidden risk

For chronic conditions, maintaining prescriptions is often the first practical hurdle: a familiar brand may not be available locally, formulations can differ, and some medicines are subject to import controls. Travel and border rules can require proof of prescription and careful packing, particularly for liquids, injectables, or controlled medicines.[9]

This guide focuses on insurance mechanics and planning. It doesn’t provide medical advice or recommend treatment; for health decisions, rely on qualified clinicians.

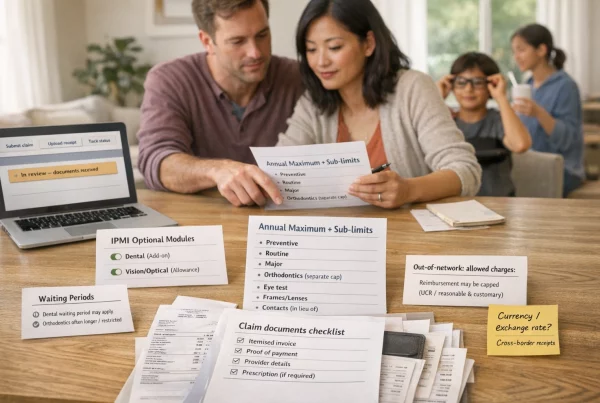

What IPMI covers (in-patient, out-patient, medications)

International private medical insurance is typically built around in-patient (hospital) benefits, with optional or tiered additions for out-patient care and prescription medicines. For chronic conditions, those optional elements often determine whether the cover is workable day-to-day.

Usually the “core” of IPMI: admissions, surgery, overnight stays, and some specialist procedures. Planned admissions commonly require pre-authorisation and may need the facility and lead consultant/surgeon named on the request.

Consultations, tests, imaging, therapies and follow-up outside hospital. For chronic illness insurance, check visit limits, annual limits, and whether diagnostics have separate caps or sub-limits.

Often variable: may be included, optional, or limited. Look for formulary rules, prior authorisation, quantity limits, and whether “specialty” medicines are handled differently.[4]

In-patient: where “covered” can still mean “managed”

Even with strong in-patient cover, insurers typically manage planned admissions through pre-authorisation. That isn’t necessarily a problem — it’s how insurers confirm eligibility, coordinate direct billing, and reduce avoidable disputes later. But it does mean you (or a caregiver) should treat approvals as part of the treatment timeline, not an afterthought.

Out-patient: the budget line many people underestimate

Chronic conditions often involve a predictable rhythm: specialist reviews, blood tests, imaging and prescription renewals. If a policy’s out-patient limits are low (or out-patient cover is excluded), you may end up funding a significant share of routine care while still paying a premium.

What to check in out-patient benefits:

- Annual out-patient limit and whether it resets each policy year.

- Sub-limits for diagnostics (blood tests/imaging), therapies, or specialist consultations.

- Referral requirements (some insurers require a GP referral even if the local system doesn’t).

- Chronic monitoring (e.g., regular blood tests, scans) and whether it’s treated differently from acute consultations.

Medications: formularies, tiers, and prior authorisation

Many health plans use a formulary — a covered drug list — and apply rules such as prior authorisation (and, in some markets, step-therapy-type requirements). At a high level, this is a form of utilisation management: insurers seek to ensure appropriate use and manage costs, particularly for high-cost medicines.[4]

In practical terms, this can affect expats taking high-cost medicines, biologics, some cancer therapies, specialist injectables, or medicines prescribed “off-label”. Your policy may require supporting documentation from your treating clinician and may limit cover to specific indications or quantities.[4]

It’s easy to assume that if hospital treatment is covered, all related ongoing medication will be covered automatically. In reality, in-patient and out-patient prescription benefits can sit separately, and some plans treat long-term “maintenance” prescriptions differently from short courses linked to acute episodes. Always check how ongoing prescriptions are handled under your specific policy (formulary position, limits/sub-limits, and any approval requirements).

What about long-term care?

“Long-term care cover” can mean different things across countries and insurers. Some medical policies focus on diagnosis, treatment and recovery, while longer-term support with daily living (home assistance, residential care) may be limited, excluded, or arranged separately. Treat long-term care as a priority “verify” item rather than assuming it sits within standard IPMI.

Where travel insurance fits (and usually doesn’t)

Travel insurance is designed for short trips and emergencies. It usually isn’t intended to operate as chronic illness insurance for routine management abroad. If you’re relocating, relying on travel cover for diabetes abroad, cancer follow-up, or ongoing prescriptions commonly leads to gaps. Use travel cover as a temporary bridge only where it’s clearly appropriate and you understand the exclusions and conditions.

Underwriting and exclusions

Underwriting is where a policy becomes “real” for chronic conditions. Two people can buy cover under the same brand and end up with materially different outcomes because the offered terms differ. It’s also where vague assumptions (“they cover pre-existing conditions”) can create the biggest risk.

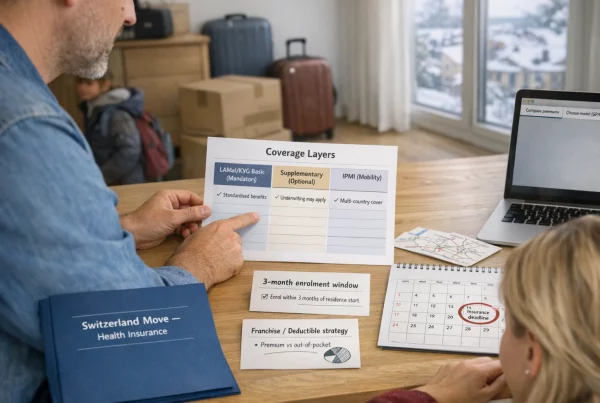

Two common approaches: full medical underwriting vs moratorium-style

Many international plans use either full medical underwriting (FMU) or a moratorium approach for pre-existing conditions. FMU usually involves disclosing your medical history and receiving terms (such as exclusions or loadings) based on that disclosure. Moratorium approaches commonly exclude pre-existing conditions for a period, and some conditions may become covered later if defined symptom-/treatment-free criteria are met, depending on the policy rules.[1]

| Underwriting approach | What it often looks like in practice | Why it matters for chronic conditions |

|---|---|---|

| Full medical underwriting (FMU) | You disclose your history; the insurer offers terms (e.g., standard terms, exclusions, medical loading). The aim is clarity on what is and isn’t covered from inception.[1] | Can provide more certainty for ongoing care — but may come with exclusions or higher premiums. Decisions can take longer where additional medical evidence is needed. |

| Moratorium-style underwriting | Pre-existing conditions are excluded initially; some may become covered later if you meet defined criteria over a set period. Exact rules vary by insurer and policy wording.[1] | Often unsuitable if you expect regular treatment or medication in the early years, because ongoing care can keep the moratorium in force. |

Exclusions, loadings, and special terms

An insurer may exclude a condition entirely, offer cover with a medical loading, or apply other special terms. Definitions matter: an “exclusion” means the insurer will not pay claims for that condition (as defined in the policy wording).[2] A “medical loading” generally means an additional premium due to health-related risk factors.[2]

In practical terms, you need to understand the offered terms before you rely on them. If a chronic condition is excluded, it may not be limited to the “main” treatment — related diagnostics, complications, and follow-up can fall within the scope of the exclusion wording.

Disclosure: small omissions can create significant claims issues

If you’re applying for IPMI, treat the medical questionnaire as a formal disclosure document, not a tick-box exercise. Insurers expect accurate and complete information. If something relevant is omitted and later links to a claim, you can face delays, requests for records, or a dispute about cover. If you’re unsure whether something is relevant (symptoms, investigations, medication), it’s usually safer to disclose and ask how it will be treated.

- List conditions, symptoms, and investigations in date order (even if resolved).

- Include medication history (including “as required” medicines) and why each was prescribed.

- Attach key reports if you have them (clinic letters, imaging summaries, discharge notes).

- Ask the insurer to confirm the terms in writing (for example, on the certificate of insurance and any special terms letter/endorsement).

Waiting periods and benefit-specific limitations

Even where a condition isn’t excluded, you may see waiting periods for specific benefits (or limitations on certain categories of care). In chronic scenarios, these are often most visible in out-patient therapies, mental health benefits, or optional modules. Always cross-check the benefits schedule and policy wording, not just marketing summaries.

Accessing specialist care and networks

For chronic conditions, “access” means two things: can you see the right specialist at the right cadence, and can your insurer and the provider work together smoothly? Provider networks, referral expectations, and billing practices can make the difference between predictable admin and repeated friction.

Provider networks: why they matter beyond price

Networks aren’t just discount lists. They often determine whether direct billing is available, whether a hospital will request a guarantee of payment, and how much back-and-forth you’ll face over documentation.

- In-network care often makes direct billing more achievable (but it isn’t automatic; authorisation may still be required).

- Out-of-network care may require you to pay first and claim back, sometimes subject to “reasonable and customary” limits.

- Split billing is common: the hospital may bill the insurer, but individual clinicians (radiologist, anaesthetist, laboratory) bill you separately.

Specialist access: reducing “wrong door” appointments

If you have a complex condition (for example, an autoimmune condition requiring specialist follow-up), do a basic access check before you move: identify at least two suitable specialists and confirm how they bill. You’re not selecting a clinic here — you’re checking that the network has realistic options and that the admin pathway is workable.

Hi — I have international private medical insurance. Before I book, can I check your billing process? 1) Do you accept direct billing / direct settlement with international insurers? 2) If not, can you provide an itemised invoice and proof of payment after the appointment? 3) Will the invoice include the clinician’s name, date of service, and a clear description of services/tests? 4) If the insurer requests additional documents (referral letter, report), who can provide them and how quickly?

Use the contact details shown in your policy documents, member portal/app or member card for insurer-specific instructions — don’t rely on informal phone numbers found online.

Pre-authorisation and specialist pathways

Many plans require pre-authorisation for higher-cost diagnostics (MRI/CT), procedures, admissions, or specialty medicines. Some plans also require a referral letter to support specialist consultations, even if the local system allows self-referral. Prior authorisation is a common utilisation management tool, particularly for prescription benefits.[4]

Hi — I’m a member and I’m planning ongoing care abroad. I have [condition] and I expect regular [specialist] reviews and [tests/medications]. Can you confirm: 1) Whether my condition is covered on my current terms (or whether any exclusions/special terms apply). 2) Which services require pre-authorisation (specialist visits, scans, admissions, high-cost medicines). 3) Which providers are in-network where I live, and whether direct billing is available. 4) What documents you need (referral letter, treatment plan, recent results) and how to submit them securely.

Practical tip: keep a “billing-ready” file

One of the simplest ways to reduce delays is to keep a small set of documents ready: your policy number, a short medical summary, current prescriptions, and recent clinic letters. Where pre-authorisation is required, supplying clear information up front reduces back-and-forth.

Comparing local vs international solutions

Many expats compare local private plans, state healthcare (where they’re eligible), and IPMI. There’s no universal “best” choice — the right set-up depends on residency rules, where you will realistically receive care, and how much portability you need. For chronic conditions, the deciding factors are usually: certainty of cover, access to medicines, specialist availability, and cross-border continuity.

| Option | What it can work well for | Typical trade-offs to watch |

|---|---|---|

| Local private insurance | Strong local networks; sometimes simpler local billing and access to local prescriptions. Can be cost-effective in some markets. | Often limited outside the country; portability may be weak if you move again. Underwriting rules and the way chronic conditions are handled can vary significantly. |

| State healthcare (where eligible) | May provide broad access for long-term conditions and ongoing care, depending on eligibility and system capacity. | Eligibility can be strict; waiting times and referral routes may differ from private care. A private “top-up” may still be used for speed or choice. |

| IPMI (international private medical insurance) | Portability across countries; support for internationally mobile families. Often useful where you want access to private care and more consistent admin across multiple locations. | Pre-existing condition terms can be decisive; prescription benefits vary; networks may be stronger in some regions than others. Long-term care may be limited or excluded. |

When a “hybrid” approach is considered

Some families combine solutions — for example, a local plan to integrate with the local system plus an international layer for travel or future relocations. If you go down this route, map out what each layer covers and, crucially, what each one excludes. Overlaps can be inefficient, but gaps can be expensive.

Long-term care: assume separate planning may be needed

If an ageing parent may need home care or assisted living, treat this as a planning stream alongside medical insurance. Medical policies generally focus on diagnosis and treatment; ongoing day-to-day support often sits in a different category and may require separate budgeting or arrangements. It’s better to clarify definitions and limits early than discover them in a crisis.

Continuity of care when relocating

Continuity of care is the “invisible infrastructure” that helps keep chronic conditions stable during a move: coordinated care, smooth handovers, and records that are actually usable across clinicians.[7] Insurance doesn’t replace this — but good continuity planning can make insurer admin quicker and reduce the risk of prescription gaps.

Before you move: build a portable medical summary

If you do one thing, do this: ask your clinician for a brief letter summarising your diagnoses, medicines (generic names and doses), allergies, and any essential equipment. Travel health guidance recommends carrying this kind of letter and keeping medicine information accessible.[8]

- Keep it short: 1–2 pages is usually enough for an initial handover.

- Use generic names: brand names vary by country; generic names help pharmacies and clinicians identify equivalents.[8]

- Attach key results: recent relevant bloods, imaging summaries, and clinic letters (not your full history unless asked).

- Translate essentials: if you’re moving into a different language environment, translate your medicines list and diagnosis summary where practical.

Medication continuity: plan refills like a supply chain

Prescription access problems rarely show up on day one — they appear when you hit your first refill cycle abroad. Aim to arrive with enough supply for the transition period and keep medicines in original packaging with prescriptions/letters where needed.[9]

- Carry enough medication for the trip plus a buffer for delays, and keep it in your hand luggage where possible.[8]

- Keep medicines and devices in original packaging; carry a copy of your prescription and consider whether a translation may be needed.[9]

- Rules can be stricter for certain medicines (especially controlled drugs); check the destination country’s requirements and keep documentation ready.

Insurance continuity: avoiding “mid-treatment” surprises

If you’re relocating mid-treatment (or expect planned follow-up soon after arrival), align the admin timeline with the clinical one: identify what needs pre-authorisation, what may be reimbursed, and what is most sensitive to delays (for example, specialty medicine approvals).

Practical steps:

- Notify the insurer of any address/country changes where your policy requires it.

- Ask what documentation is needed from your current clinician to support ongoing care abroad.

- Confirm the provider network in your new location and the process for booking in-network care.

- For high-cost medicines, confirm the formulary position and the prior authorisation route in the new country.[4]

Privacy: treat health data as sensitive by default

Health information is treated as sensitive (“special category”) personal data under data protection frameworks, which requires additional safeguards.[11] Use secure insurer channels (member portals, secure upload links, official helplines) and avoid oversharing: provide what’s necessary for underwriting or claims, rather than sending your full history unless it’s requested.

Common pitfalls (and how to avoid them)

These are the issues we see most often when expats plan chronic care abroad:

Travel cover is usually not designed for routine chronic management. Treat it as emergency/short-term protection only, and check exclusions carefully.

Formulary checks, prior authorisations, and refill timing can be the difference between a smooth month and a stressful one.[4]

You may have to pay up front and reimbursement may be limited. Confirm network status and billing before booking wherever possible.

Incomplete medical history can trigger delays and disputes at claims stage. If in doubt, disclose and ask how it will be treated under the policy.

Availability and naming vary; plan refills and carry documentation, including generic names.[9]

A hospital may bill the insurer but individual clinicians/labs may bill you. Ask for itemised invoices and keep proof of payment.

Missing referral letters, unclear invoices, or untranslated summaries can slow approvals and claims. Keep a “billing-ready” file.

Case examples (decision logic, not promises)

These anonymised scenarios show how to think through options without assuming guaranteed outcomes. They focus on process: what to verify, what to prepare, and what to prioritise.

You need reliable access to prescriptions, monitoring supplies, and periodic reviews. Key checks are out-patient benefits (specialist visits, blood tests) and pharmacy benefits (insulin/medicines, and supplies where applicable).

- Check whether diabetes is covered on the terms offered (or excluded/loaded) and how routine monitoring is treated.

- Confirm prescription rules: formulary status, refill quantities, and whether any items require prior authorisation.[4]

- Build a refill plan and carry a clinician letter with generic names and doses to support border/admin requirements.[8]

You may be managing surveillance, periodic tests, and a need for rapid access if symptoms return. The core question is what counts as “pre-existing” under the policy, and how follow-up investigations are treated.

- Clarify the underwriting approach and any cancer-related exclusions or special terms; confirm how follow-up scans are handled.

- Map network access to relevant oncology services in the destination city and how direct billing works in practice.

- Ask what triggers pre-authorisation (imaging, admissions, specialty medicines) and what evidence is required for approvals.[4]

The policy must support regular specialist reviews, monitoring bloods, and potentially high-cost medicines. This is where formulary and prior authorisation processes become central.

- Confirm out-patient limits and whether monitoring has specific caps or sub-limits.

- Check how specialty medicines are handled: formulary inclusion, prior authorisation steps, and documentation requirements.[4]

- Plan continuity: carry a concise treatment history and recent results to help re-establish care more quickly.[7]

If the primary need is help with day-to-day living, a standard medical policy may not be the right tool. The planning question is what “long-term care” benefits exist (if any), and what needs to be arranged separately.

- Clarify how the policy defines long-term care, and whether home nursing, carers, or residential support are included, limited, or excluded.

- Separate “medical treatment” (diagnosis, hospital care) from “support needs” (assistance with daily living) when budgeting.

- Check local service availability and the billing approach (direct billing vs reimbursement) if any relevant benefits apply.

Checklist for patients and caregivers

Whether you’re managing a chronic condition yourself or supporting a partner, child or parent, the aim is straightforward: reduce avoidable admin, reduce avoidable financial shocks, and reduce avoidable treatment gaps. This checklist is intended to be practical — not perfect.

- A one-page medical summary: diagnoses, allergies, key procedures, and your current care plan.

- A medication list with generic names, doses, timing, and purpose; include “as required” medicines too.

- Recent clinic letters and key test results (last 12–24 months, or as relevant).

- Translations of essentials if moving into a different language environment (medication list + diagnoses).

- Arrive with enough supply for the transition plus a buffer; pack in line with travel guidance (hand luggage, original packaging).[9]

- A clinician letter for travel/admin, especially for injectables, liquids, devices, or controlled medicines.[8]

- A refill plan: local prescriber appointment timing, pharmacy options, and insurer processes for specialty medicines.

- Policy number, member ID card, and official insurer contact routes saved (portal/app/helpline).

- A clear understanding of deductibles/excesses and co-payments, and how direct billing vs reimbursement works.

- A list of likely pre-authorisation triggers for your care (scans, admissions, high-cost medicines).

- A simple “claims folder” for invoices, receipts, referral letters, and proof of payment.

- Local emergency numbers and a plan for where you would go first if symptoms escalate.

- Caregiver permissions: who can speak to the insurer/provider if you’re unwell (where local rules allow).

- Secure storage for sensitive documents; share only what’s needed via secure channels.[10]

Questions to ask (before you buy, and again when you relocate)

A) Questions for insurers / administrators (chronic conditions + high-cost medicines)

| Topic | Questions to ask | Why it matters |

|---|---|---|

| Pre-existing conditions | How do you define “pre-existing”? Which underwriting approach applies (full medical vs moratorium)? What special terms (exclusions/loadings) would apply to my history?[1] | Determines whether your condition can be covered, excluded, or restricted — and when. |

| Out-patient chronic care | Are specialist consultations, blood tests, imaging, and ongoing monitoring covered? Are there caps or sub-limits for diagnostics/therapies? | Chronic care is often out-patient-heavy; limits can shift costs back to you. |

| Prescription benefit | Is out-patient medication included? Is there a formulary? Are there annual limits, tiers, or quantity limits? | Prescription costs can be significant — especially for specialty medicines. |

| Prior authorisation | Which services need pre-authorisation (scans, admissions, specialty medicines)? How do I submit requests and what documents are required?[4] | Missing authorisation can delay settlement and create avoidable stress. |

| Networks and billing | Which providers are in-network in my destination city? Where is direct billing available? If I go out-of-network, how is reimbursement calculated? | Affects upfront costs and the admin burden for regular appointments. |

| Portability and relocation | What changes if I relocate (territory, premium, network)? How do claims work if I move mid-treatment? | Continuity planning depends on whether terms and access remain consistent across moves. |

| Long-term care | How does the policy define long-term care? Is home care/assisted living included, limited, or excluded? Is it an optional benefit or a separate arrangement? | Long-term support is commonly misunderstood; definitions and limits are critical. |

B) Questions for providers (continuity + billing admin)

| Topic | Questions to ask | Why it matters |

|---|---|---|

| Continuity handover | Can you accept records electronically? Do you provide visit summaries in English (or can you provide a short summary suitable for insurers)?[7] | Better documentation improves coordination and can reduce duplication. |

| Billing model | Do you direct bill international insurers? If not, can you provide itemised invoices and proof of payment? Who issues these (clinic vs clinician)? | Determines whether you need to pay up front and how straightforward claims submission will be. |

| Estimates and authorisation | Can you provide a written estimate for planned care and help supply the documents needed for insurer pre-authorisation? | Pre-authorisation often depends on clear clinical and cost information. |

| Follow-up cadence | What is the typical review schedule for my condition, and which tests are usually used for monitoring? | Helps you plan costs and admin (without assuming clinical outcomes). |

| Prescribing process | Will you prescribe using generic names? Can prescriptions be issued in a format local pharmacies accept? | Reduces friction where brand names and formats differ across countries. |

Broker support

Choosing expat insurance for chronic conditions isn’t just about comparing premiums. It’s about understanding how underwriting, networks, prescription rules, and admin workflows will affect your day-to-day experience. This is where a specialist broker can help you assess options and avoid mismatched expectations.

What we can do (and what we can’t)

As brokers, we can help you interpret policy wording, compare benefit structures, and plan the admin steps that reduce risk. We can also help you prepare disclosures and ask the right verification questions before you commit. Claims decisions sit with the insurer (based on the policy terms), and clinical decisions sit with your treating clinicians — but having support from someone who understands the process can reduce delays and confusion.

Clarify how pre-existing conditions are assessed, how out-patient and prescription benefits work, and where the likely friction points are.

Build a practical plan for pre-authorisations, provider selection, billing routes, and documentation — before you’re under pressure.

Help you navigate insurer processes, track documentation requirements, and reduce avoidable delays for planned care.

Get Started

If you’re planning a move (or already abroad) and want a structured way to compare international cover for chronic conditions, start with our Individual & Families page. If you have practical questions about how IPMI works, billing, and next steps, our FAQ is a useful reference point.

Further reading: For a deeper look at underwriting mechanics (including full medical vs moratorium-style approaches), see How underwriting works in international health insurance (IPMI). If you’re still planning the move and want a broader relocation checklist, read IPMI Abroad: The Guide to Getting Health Cover Right Before You Move.

Points to verify

The items below can vary materially by insurer, policy, country, and provider. Treat this as a due-diligence checklist before you rely on cover — particularly for high-cost medicines and specialist care.

- How pre-existing conditions are assessed: full medical vs moratorium-style approaches; what is excluded, loaded, or accepted; and what evidence is required.[1]

- Out-patient prescription cover: whether it’s included or optional; formulary rules; tiers; quantity limits; and how prior authorisation works for high-cost medicines.[4]

- Cover for chronic monitoring: specialist consultations, blood tests, imaging; any caps or sub-limits; and whether monitoring is treated differently from acute consultations.

- Network access: in-network specialists and centres in your destination; referral requirements (if any); and how to confirm direct billing status.

- Direct billing vs reimbursement: when direct billing applies; when you may need to pay up front; and what documents are needed for reimbursement claims.

- Emergency vs planned care rules: what requires pre-authorisation; notification windows; and what happens when you can’t obtain approval in advance.

- Long-term care definitions and limits: what “long-term care” means under your policy; whether it’s excluded, capped, or separate/optional; and how home care/assisted living is treated.

- Cross-border portability: territorial scope; whether premium/terms change when you relocate; and how claims work when moving mid-treatment across countries.

- Documentation requirements: translations, itemised invoices, referral letters, proof of payment, claim submission time limits, and accepted submission channels.

- Privacy and secure sharing: which official channels the insurer provides for sensitive health data; minimise unnecessary sharing and keep your own records secure.[10]